January 31, 2017

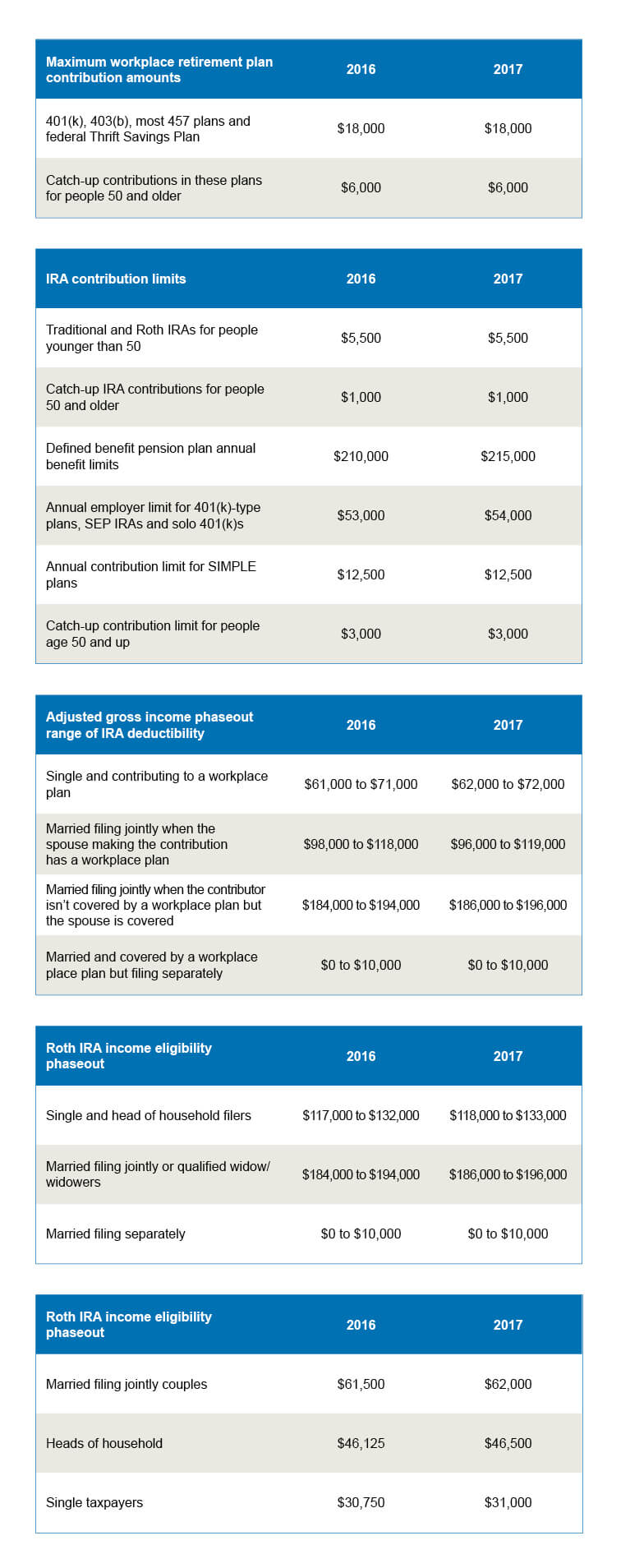

For years, the amount of money the government would allow Americans to stow away for retirement has been the same with very little fluctuation. The year 2017 however will bring some fresh changes to your 401(k), 403(b) and most government plans.

While some government limitations will not change, others will and they are worth paying attention to. For instance, if you’re lucky enough to be covered by a traditional pension plan at work, the maximum amount you can collect as an annual benefit has increased from $210,000 to $215,000. What’s more, if your employer makes contributions to your 401(k)-type plan, the maximum that can be contributed annually rose to $54,000 a year from $53,000. These changes and limits apply to self-employed entrepreneurs as well.

To help clients, prospects and others understand the limitations, Wilson Lewis has outlined the new 2017 IRS changes below. The changes include income limits for those who contribute to both a traditional IRA and a workplace retirement plan (or those whose spouses have access to a workplace plan), as well as the income limits for those who contribute to Roth IRAs. It is noteworthy to add that middle- and low-income savers may qualify for a saver’s credit that can be worth up to $2,000.

Contact Us

These changes represent an opportunity for additional retirement savings where possible. If you have any questions regarding pension plans and their limitations or would like assistance with wealth and retirement planning, Wilson Lewis can help. For additional information, please call us at 770-476-1004, or click here to contact us.