December 27, 2020

Atlanta businesses looking for last-minute options to increase cash flow before the end of the year may be in luck. The CARES Act, passed earlier this year, contained several tax benefits and incentives to help struggling businesses create a capital infusion. While the list is comprehensive there was one change that offers significant savings benefit, the temporary expansion of Net Operating Losses (NOLs). The changes highlighted in the CARES Act apply to tax years 2018, 2019, and 2020, include a 5-year lookback period, an unlimited carryforward period, and expanded access for pass-through entities including partnerships and S-corporations. It not only expands the potential savings but opens the door for additional businesses to participate. To help clients, prospects, and others, Wilson Lewis has provided a summary of the key details below.

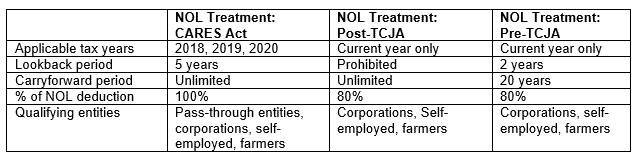

The term ‘regular’ is a bit of a misnomer, considering how much NOL treatment has changed in the past few years. To get a better sense of what’s changed, compare the CARES Act treatment of NOL carrybacks to two previous periods: pre-and post-Tax Cuts and Jobs Act (TJCA).

Prior to January 1, 2018, NOLs were permitted to look back up to two years with a maximum deduction of 80 percent of adjusted taxable income. TCJA prohibited NOL carrybacks altogether; losses had to be claimed in the same year they were incurred. Both periods prohibited pass-through entities from electing NOL treatment.

A side-by-side comparison of the major changes is listed below.

It is easy to see that the CARES Act relaxed several aspects of the NOL election to give businesses quicker access to cash flow amidst COVID-19. Three major changes new this year include:

The ability to look back five years gives businesses more leeway in applying the tax deduction from previous losses to offset tax liability now. Plus, now that pass-through entities are allowed to claim NOL carrybacks, more businesses can participate than before. According to the IRS, “Partnerships and S corporations generally cannot use an NOL. However, partners or shareholders can use their separate shares of the partnership’s or S corporation’s business income and business deductions to figure their individual NOLs.”

Further, any year in which a business incurred foreign income under Section 965 can be excluded from NOL treatment.

Earlier in 2020, businesses had the opportunity to look back to 2017 and 2018 under a special CARES Act rule, but the deadlines have since passed. Now, at year-end, the remaining options are to look back to 2018, 2019, or the current year.

Considering that corporate income taxes were higher before TCJA was passed and pass-through entities are now allowed to claim the deduction, an NOL carryback election could generate a substantial refund.

To make the NOL election, file Form 1139 (Corporations) or 1145 (all other taxpayers) or file an amended return. For prior years, businesses could receive a refund within about 90 days. For losses incurred in 2020, the refund will come after the annual return is completed and filed. Any year in which the taxpayer was, or is, a REIT disqualifies the NOL election.

Businesses can also elect to revoke a previous NOL election and instead carry those losses forward to future years. Deciding whether to take the deduction in 2019, 2020, or carry the loss forward depends on individual circumstances.

Losses from business operations, theft, casualties, moving expenses, rental property, and certain other deductions generally all qualify for NOL. Items that do not apply when calculating the deduction include:

Contact Us

The expanded NOL carryback rules create a compelling tax savings opportunity. Given the complexity of the regulations, it is important to consult with a qualified tax advisor to determine the best path forward. If you have questions about NOL carrybacks or need assistance with another tax or accounting issue, Wilson Lewis can help. For additional information call us at 770-476-1004 or click here to contact us. We look forward to speaking with you soon.

Notifications